If you have a half-finished kitchen in Jonesborough or a master suite addition in Kingsport that’s been "stuck" for six months, you aren't just living in a construction zone—you are living in an insurance gray area. Many homeowners assume that as long as they pay their premiums, any damage to their home is covered. However, standard home insurance policies are designed for completed, occupied dwellings, not active (or abandoned) construction sites.

When a project stalls, the risk profile of your home changes entirely. From exposed wiring that poses a fire hazard to open structures that invite "attractive nuisance" liability claims, an unfinished project can trigger "material change in risk" exclusions. This means if a claim occurs, your carrier might have grounds to deny it because the home was not in the condition they originally agreed to insure.

At Veritas Risk Management, we believe in "Real Intelligence." That means telling you the truth before the storm hits. Our goal is to help you navigate these transitions safely, ensuring that your most valuable asset is protected even when the hammers stop swinging.

The Stalled Classic Car: Why Your Home Isn't Just "A Little Messy"

Imagine you bought a beautiful 1967 Mustang. You insured it as a daily driver because it was pristine and safe. Then, you decided to restore it. You pulled out the engine, stripped the brakes, and left it sitting on blocks in the driveway for a year. If you tried to file a claim because it rolled away or caught fire, the insurance company would likely point out that you aren't driving the car they insured. You’re now "storing" a project.

Your Tennessee home works the same way. When you start a major renovation, you are essentially "pulling the engine" out of your house. A home with no kitchen sink, exposed wall studs, or a tarp for a roof is no longer a standard "owner-occupied dwelling" in the eyes of an actuary. It is a "material change in risk."

At Veritas, we see our clients as neighbors, not policy numbers. We know life happens—contractors disappear, budgets get tight, or maybe you just ran out of steam on that DIY deck in Elizabethton. But leaving that project in limbo without talking to your agent is like driving that Mustang without brakes.

Why "Almost Done" Isn't Good Enough for Your Carrier

The "Material Change in Risk" Clause

Every insurance policy contains language regarding a "material change in risk." This is a fancy way of saying: "If the house becomes significantly more dangerous to insure than it was when we signed the contract, you have to tell us." An unfinished project—especially one involving structural changes, electrical, or plumbing—is the definition of a material change.

Property Value vs. Replacement Cost

If you’ve added 500 square feet to your home in Gray but haven't finished the interior, what is the house worth? If a fire occurs, do you get the value of the old house or the value of the new, unfinished one? Without a "Builder's Risk" endorsement or a policy update, you may find yourself underinsured, leaving you to foot the bill for thousands of dollars in materials and labor already invested.

The Three Pillars of Risk in Unfinished Projects

The Liability Trap: Open Subfloors and Exposed Wiring

Tennessee hospitality means neighbors stop by. But if a neighbor or a delivery driver trips on an exposed subfloor in your unfinished mudroom, your standard liability insurance might be called into question. Construction sites are inherently dangerous. If the project is stalled, those dangers persist longer than intended, increasing the statistical likelihood of an accident.

Theft and Vandalism: Why Unsecured Sites are Targets

Unfinished homes often have unsecured entrances or valuable materials (like copper piping or new appliances) sitting in plain sight. Most standard policies have limits on "theft of building materials" if the home is under renovation. If your Greeneville project is sitting idle, it becomes a magnet for trouble.

Structural Integrity: Weathering the Tennessee Elements

We all know how unpredictable the weather can be in the Tri-Cities. A roof that is "dried in" with felt paper is meant to last a week, not a whole winter. If water seeps in and causes mold because a project stalled, many carriers will deny the claim based on "failure to maintain the property."

Local Spotlight: Real-World Scenarios in the Tri-Cities

- The Rogersville Kitchen: A family started a total kitchen gut. The contractor walked away, leaving live wires capped but exposed and no working plumbing. A small leak from a temporary pipe caused massive floor damage. Because the "risk" had changed and the home was partially gutted, the claim process became a nightmare.

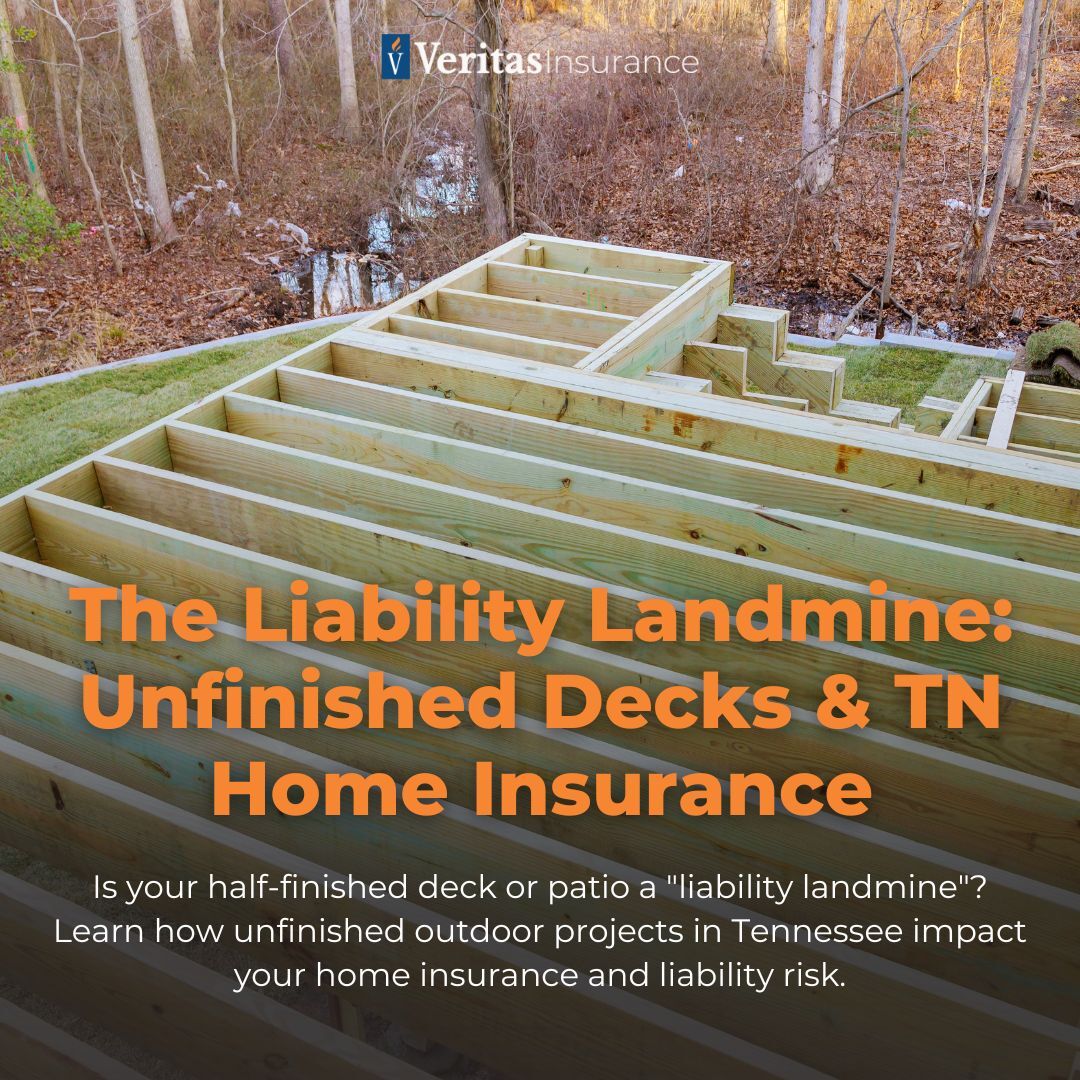

- The Bluff City Deck: A homeowner started a massive multi-level deck. He stopped after the framing but before the railings were installed. During a summer BBQ, a guest fell off the edge. This is a classic "attractive nuisance" that could have been mitigated with proper umbrella insurance.

How to Bridge the Gap: Steps to Take Today

- Be Honest: Call us. We aren't here to judge your unfinished project; we’re here to protect you. Honesty and accountability are our core values.

- Ask about Builder's Risk: Even for renovations, a "Builder's Risk" or "Course of Construction" policy (often through carriers like Builders Mutual) can provide the specific protection you need while the home is in flux.

- Secure the Site: If a project is stalled, board up windows, lock gates, and remove high-value tools or appliances.

- Document Everything: Take photos of the progress. This helps us advocate for you with the carrier if a claim arises.

Cross-Coverage Connection: Beyond the Roof and Walls

Risk management isn't just about the structure; it's about the people inside.

Why an Umbrella Policy is Your Safety Net

When your home is a construction zone, your "surface area" for a lawsuit grows. A personal umbrella policy provides an extra layer of protection (usually starting at $1 million) that kicks in if your primary home liability is exhausted. In a world of rising legal costs, it's the ultimate "sleep better at night" coverage for any TN homeowner.

Protecting the Provider: The Role of Life Insurance

If you are mid-renovation and something happens to the primary breadwinner, would your family be left with a half-finished, unsellable house and a construction loan? Life insurance ensures that your family has the funds to complete the project or pay off the mortgage, turning a potential disaster into a managed transition. We believe in supportive relationships—and there is no greater support than ensuring your family’s home is finished and safe.

The Veritas Promise

At Veritas Risk Management, we don't just sell policies; we provide "Real Answers." Whether you are insured with Erie Insurance, Progressive, or Aflac, our team is dedicated to taking ownership of your insurance challenges. We serve the families of Johnson City, Kingsport, and the surrounding areas with the empathy and integrity you deserve.

Don't let an unfinished project become a finished claim.

Contact Us Today:

Johnson City Office 4451 North Roan Street, Suite #201 Johnson City, TN 37615 Phone: 423-292-4142

Kingsport Office 419 E Market St Kingsport, TN 37660 Phone: 423-328-8434

Online: https://veritasrm.com

Author: Andrew Darlington

Andrew Darlington is the founder and president of Veritas Risk Management & Insurance Services. With nearly 30 years in the industry, Andrew holds prestigious designations including CIC, CRM, AAI, and CBIA. His unique background in accounting fuels his analytical approach to risk and his competitive drive to find the best solutions for his clients. A long-time resident of East Tennessee, Andrew is committed to "serving Christ by serving others first."

Andrew Darlington

Andrew Darlington